Perspectives on Inequality and Opportunity from the Survey of Consumer Finances

The distribution of income and wealth in the United States has been widening more or less steadily for several decades, to a greater extent than in most advanced countries.1 This trend paused during the Great Recession because of larger wealth losses for those at the top of the distribution and because increased safety-net spending helped offset some income losses for those below the top. But widening inequality resumed in the recovery, as the stock market rebounded, wage growth and the healing of the labor market have been slow, and the increase in home prices has not fully restored the housing wealth lost by the large majority of households for which it is their primary asset.

The extent of and continuing increase in inequality in the United States greatly concern me. The past several decades have seen the most sustained rise in inequality since the 19th century after more than 40 years of narrowing inequality following the Great Depression. By some estimates, income and wealth inequality are near their highest levels in the past hundred years, much higher than the average during that time span and probably higher than for much of American history before then.2 It is no secret that the past few decades of widening inequality can be summed up as significant income and wealth gains for those at the very top and stagnant living standards for the majority. I think it is appropriate to ask whether this trend is compatible with values rooted in our nation’s history, among them the high value Americans have traditionally placed on equality of opportunity.

Some degree of inequality in income and wealth, of course, would occur even with completely equal opportunity because variations in effort, skill, and luck will produce variations in outcomes. Indeed, some variation in outcomes arguably contributes to economic growth because it creates incentives to work hard, get an education, save, invest, and undertake risk. However, to the extent that opportunity itself is enhanced by access to economic resources, inequality of outcomes can exacerbate inequality of opportunity, thereby perpetuating a trend of increasing inequality. Such a link is suggested by the “Great Gatsby Curve,” the finding that, among advanced economies, greater income inequality is associated with diminished intergenerational mobility.3 In such circumstances, society faces difficult questions of how best to fairly and justly promote equal opportunity. My purpose today is not to provide answers to these contentious questions, but rather to provide a factual basis for further discussion. I am pleased that this conference will focus on equality of economic opportunity and on ways to better promote it.

In my remarks, I will review trends in income and wealth inequality over the past several decades, then identify and discuss four sources of economic opportunity in America–think of them as “building blocks” for the gains in income and wealth that most Americans hope are within reach of those who strive for them. The first two are widely recognized as important sources of opportunity: resources available for children and affordable higher education. The second two may come as more of a surprise: business ownership and inheritances. Like most sources of wealth, family ownership of businesses and inheritances are concentrated among households at the top of the distribution. But both of these are less concentrated and more broadly distributed than other forms of wealth, and there is some basis for thinking that they may also play a role in providing economic opportunities to a considerable number of families below the top.

In focusing on these four building blocks, I do not mean to suggest that they account for all economic opportunity, but I do believe they are all significant sources of opportunity for individuals and their families to improve their economic circumstances.

Income and Wealth Inequality in the Survey of Consumer Finances

I will start with the basics about widening inequality, drawing heavily on a trove of data generated by the Federal Reserve’s triennial Survey of Consumer Finances (SCF), the latest of which was conducted in 2013 and published last month.4 The SCF is broadly consistent with other data that show widening wealth and income inequality over the past several decades, but I am employing the SCF because it offers the added advantage of specific detail on income, wealth, and debt for each of 6,000 households surveyed.5 This detail from family balance sheets provides a glimpse of the relative access to the four sources of opportunity I will discuss.

While the recent trend of widening income and wealth inequality is clear, the implications for a particular family partly depend on whether that family’s living standards are rising or not as its relative position changes. There have been some times of relative prosperity when income has grown for most households but inequality widened because the gains were proportionally larger for those at the top; widening inequality might not be as great a concern if living standards improve for most families. That was the case for much of the 1990s, when real incomes were rising for most households. At other times, however, inequality has widened because income and wealth grew for those at the top and stagnated or fell for others. And at still other times, inequality has widened when incomes were falling for most households, but the declines toward the bottom were proportionally larger. Unfortunately, the past several decades of widening inequality has often involved stagnant or falling living standards for many families.

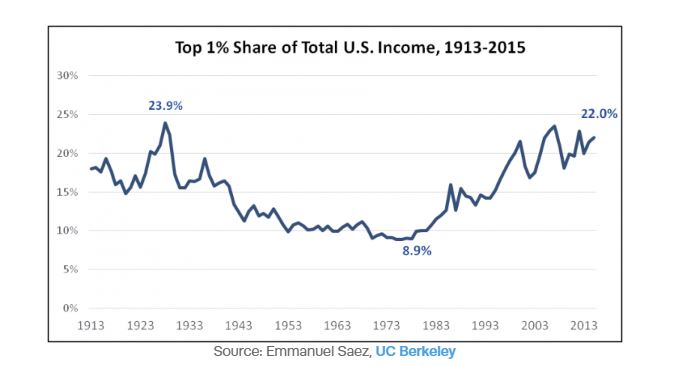

Since the survey began in its current form in 1989, the SCF has shown a rise in the concentration of income in the top few percent of households, as shown in figure 1.6 By definition, of course, the share of all income held by the rest, the vast majority of households, has fallen by the same amount.7 This concentration was the result of income and living standards rising much more quickly for those at the top. After adjusting for inflation, the average income of the top 5 percent of households grew by 38 percent from 1989 to 2013, as we can see in figure 2. By comparison, the average real income of the other 95 percent of households grew less than 10 percent. Income inequality narrowed slightly during the Great Recession, as income fell more for the top than for others, but resumed widening in the recovery, and by 2013 it had nearly returned to the pre-recession peak.8

The distribution of wealth is even more unequal than that of income, and the SCF shows that wealth inequality has increased more than income inequality since 1989. As shown in figure 3, the wealthiest 5 percent of American households held 54 percent of all wealth reported in the 1989 survey. Their share rose to 61 percent in 2010 and reached 63 percent in 2013. By contrast, the rest of those in the top half of the wealth distribution–families that in 2013 had a net worth between $81,000 and $1.9 million–held 43 percent of wealth in 1989 and only 36 percent in 2013.

The lower half of households by wealth held just 3 percent of wealth in 1989 and only 1 percent in 2013. To put that in perspective, figure 4 shows that the average net worth of the lower half of the distribution, representing 62 million households, was $11,000 in 2013.9 About one-fourth of these families reported zero wealth or negative net worth, and a significant fraction of those said they were “underwater” on their home mortgages, owing more than the value of the home.10 This $11,000 average is 50 percent lower than the average wealth of the lower half of families in 1989, adjusted for inflation. Average real wealth rose gradually for these families for most of those years, then dropped sharply after 2007. Figure 5 shows that average wealth also grew steadily for the “next 45” percent of households before the crisis but didn’t fall nearly as much afterward. Those next 45 households saw their wealth, measured in 2013 dollars, grow from an average of $323,000 in 1989 to $516,000 in 2007 and then fall to $424,000 in 2013, a net gain of about one-third over 24 years. Meanwhile, the average real wealth of families in the top 5 percent has nearly doubled, on net–from $3.6 million in 1989 to $6.8 million in 2013.

Housing wealth–the net equity held by households, consisting of the value of their homes minus their mortgage debt–is the most important source of wealth for all but those at the very top.11 It accounted for three-fifths of wealth in 2013 for the lower half of families and two-fifths of wealth for the next 45. But housing wealth was only one-fifth of total wealth for the top 5 percent of families. The share of housing in total net worth for all three groups has not changed much since 1989.

Since housing accounts for a larger share of wealth for those in the bottom half of the wealth distribution, their overall wealth is affected more by changes in home prices. Furthermore, homeowners in the bottom half have been more highly leveraged on their homes, amplifying this difference. As a result, while the SCF shows that all three groups saw proportionally similar increases and subsequent declines in home prices from 1989 to 2013, the effects on net worth were greater for those in the bottom half of households by wealth. Foreclosures and the dramatic fall in house prices affected many of these families severely, pushing them well down the wealth distribution. Figure 6 shows that homeowners in the bottom half of households by wealth reported 61 percent less home equity in 2013 than in 2007. The next 45 reported a 29 percent loss of housing wealth, and the top 5 lost 20 percent.

Fortunately, rebounding housing prices in 2013 and 2014 have restored a good deal of the loss in housing wealth, with the largest gains for those toward the bottom. Based on rising home prices alone and not counting possible changes in mortgage debt or other factors, Federal Reserve staff estimate that between 2013 and mid-2014, average home equity rose 49 percent for the lowest half of families by wealth that own homes.12 The estimated gains are somewhat less for those with greater wealth.13 Homeowners in the bottom 50, which had an average overall net worth of $25,000 in 2013, would have seen their net worth increase to an average of $33,000 due solely to home price gains since 2013, a 32 percent increase.

Another major source of wealth for many families is financial assets, including stocks, bonds, mutual funds, and private pensions.14 Figure 7 shows that the wealthiest 5 percent of households held nearly two-thirds of all such assets in 2013, the next 45 percent of families held about one-third, and the bottom half of households, just 2 percent. This figure may look familiar, since the distribution of financial wealth has concentrated at the top since 1989 at rates similar to those for overall wealth, which we saw in figure 3.15

Those are the basics on wealth and income inequality from the SCF. Other research tells us that inequality tends to persist from one generation to the next. For example, one study that divides households by income found that 4 in 10 children raised in families in the lowest-income fifth of households remain in that quintile as adults.16 Fewer than 1 in 10 children of families at the bottom later reach the top quintile. The story is flipped for children raised in the highest-income households: When they grow up, 4 in 10 stay at the top and fewer than 1 in 10 fall to the bottom.

Research also indicates that economic mobility in the United States has not changed much in the last several decades; that mobility is lower in the United States than in most other advanced countries; and, as I noted earlier, that economic mobility and income inequality among advanced countries are negatively correlated.17

Four Building Blocks of Opportunity

An important factor influencing intergenerational mobility and trends in inequality over time is economic opportunity. While we can measure overall mobility and inequality, summarizing opportunity is harder, which is why I intend to focus on some important sources of opportunity–the four building blocks I mentioned earlier.

Two of those are so significant that you might call them “cornerstones” of opportunity, and you will not be surprised to hear that both are largely related to education. The first of these cornerstones I would describe more fully as “resources available to children in their most formative years.” The second is higher education that students and their families can afford.

Two additional sources of opportunity are evident in the SCF. They affect fewer families than the two cornerstones I have just identified, but enough families and to a sufficient extent that I believe they are also important sources of economic opportunity.

The third building block of opportunity, as shown by the SCF, is ownership of a private business.18 This usually means ownership and sometimes direct management of a family business. The fourth source of opportunity is inherited wealth. As one would expect, inheritances are concentrated among the wealthiest families, but the SCF indicates they may also play an important role in the opportunities available to others.

Resources Available for Children

For households with children, family resources can pay for things that research shows enhance future earnings and other economic outcomes–homes in safer neighborhoods with good schools, for example, better nutrition and health care, early childhood education, intervention for learning disabilities, travel and other potentially enriching experiences.19 Affluent families have significant resources for things that give children economic advantages as adults, and the SCF data I have cited indicate that many other households have very little to spare for this purpose. These disparities extend to other household characteristics associated with better economic outcomes for offspring, such as homeownership rates, educational attainment of parents, and a stable family structure.20

According to the SCF, the gap in wealth between families with children at the bottom and the top of the distribution has been growing steadily over the past 24 years, but that pace has accelerated recently. Figure 8 shows that the median wealth for families with children in the lower half of the wealth distribution fell from $13,000 in 2007 to $8,000 in 2013, after adjusting for inflation, a loss of 40 percent.21 These wealth levels look small alongside the much higher wealth of the next 45 percent of households with children. But these families also saw their median wealth fall dramatically–by one-third in real terms–from $344,000 in 2007 to $229,000 in 2013. The top 5 percent of families with children saw their median wealth fall only 9 percent, from $3.5 million in 2007 to $3.2 million in 2013, after inflation.

For families below the top, public funding plays an important role in providing resources to children that influence future levels of income and wealth. Such funding has the potential to help equalize these resources and the opportunities they confer.

Social safety-net spending is an important form of public funding that helps offset disparities in family resources for children. Spending for income security programs since 1989 and until recently was fairly stable, ranging between 1.2 and 1.7 percent of gross domestic product (GDP), with higher levels in this range related to recessions. However, such spending rose to 2.4 percent of GDP in 2009 and 3 percent in 2010.22 Researchers estimate that the increase in the poverty rate because of the recession would have been much larger without the effects of income security programs.23

Public funding of education is another way that governments can help offset the advantages some households have in resources available for children. One of the most consequential examples is early childhood education. Research shows that children from lower-income households who get good-quality pre-Kindergarten education are more likely to graduate from high school and attend college as well as hold a job and have higher earnings, and they are less likely to be incarcerated or receive public assistance.24 Figure 9 shows that access to quality early childhood education has improved since the 1990s, but it remains limited–41 percent of children were enrolled in state or federally supported programs in 2013. Gains in enrollment have stalled since 2010, as has growth in funding, in both cases because of budget cuts related to the Great Recession. These cuts have reduced per-pupil spending in state-funded programs by 12 percent after inflation, and access to such programs, most of which are limited to lower-income families, varies considerably from state to state and within states, since local funding is often important.25 In 2010, the United States ranked 28th out of 38 advanced countries in the share of four-year-olds enrolled in public or private early childhood education.26

Similarly, the quality and the funding levels of public education at the primary and secondary levels vary widely, and this unevenness limits public education’s equalizing effect. The United States is one of the few advanced economies in which public education spending is often lower for students in lower-income households than for students in higher-income households.27 Some countries strive for more or less equal funding, and others actually require higher funding in schools serving students from lower-income families, expressly for the purpose of reducing inequality in resources for children.

A major reason the United States is different is that we are one of the few advanced nations that funds primary and secondary public education mainly through subnational taxation. Half of U.S. public school funding comes from local property taxes, a much higher share than in other advanced countries, and thus the inequalities in housing wealth and income I have described enhance the ability of more-affluent school districts to spend more on public schools. Some states have acted to equalize spending to some extent in recent years, but there is still significant variation among and within states. Even after adjusting for regional differences in costs and student needs, there is wide variation in public school funding in the United States.28

Spending is not the only determinant of outcomes in public education. Research shows that higher-quality teachers raise the educational attainment and the future earnings of students.29 Better-quality teachers can help equalize some of the disadvantages in opportunity faced by students from lower-income households, but here, too, there are forces that work against raising teacher quality for these students. Research shows that, for a variety of reasons, including inequality in teacher pay, the best teachers tend to migrate to and concentrate in schools in higher-income areas.30 Even within districts and in individual schools, where teacher pay is often uniform based on experience, factors beyond pay tend to lead more experienced and better-performing teachers to migrate to schools and to classrooms with more-advantaged students.31

Higher Education that Families Can Afford

For many individuals and families, higher education is the other cornerstone of economic opportunity. The premium in lifetime earnings because of higher education has increased over the past few decades, reflecting greater demand for college-educated workers. By one measure, the median annual earnings of full-time workers with a four-year bachelor’s degree are 79 percent higher than the median for those with only a high school diploma.32 The wage premium for a graduate degree is significantly higher than the premium for a college degree. Despite escalating costs for college, the net returns for a degree are high enough that college still offers a considerable economic opportunity to most people.33

Along with other data, the SCF shows that most students and their families are having a harder time affording college. College costs have risen much faster than income for the large majority of households since 2001 and have become especially burdensome for households in the bottom half of the earnings distribution.

Rising college costs, the greater numbers of students pursuing higher education, and the recent trends in income and wealth have led to a dramatic increase in student loan debt. Outstanding student loan debt quadrupled from $260 billion in 2004 to $1.1 trillion this year. Sorting families by wealth, the SCF shows that the relative burden of education debt has long been higher for families with lower net worth, and that this disparity has grown much wider in the past couple decades. Figure 10 shows that from 1995 to 2013, outstanding education debt grew from 26 percent of average yearly income for the lower half of households to 58 percent of income.34 The education debt burden was lower and grew a little less sharply for the next 45 percent of families and was much lower and grew not at all for the top 5 percent.35

Higher education has been and remains a potent source of economic opportunity in America, but I fear the large and growing burden of paying for it may make it harder for many young people to take advantage of the opportunity higher education offers.

Opportunities to Build Wealth through Business Ownership

For many people, the opportunity to build a business has long been an important part of the American dream. In addition to housing and financial assets, the SCF shows that ownership of private businesses is a significant source of wealth and can be a vital source of opportunity for many households to improve their economic circumstances and position in the wealth distribution.

While business wealth is highly concentrated at the top of the distribution, it also represents a significant component of wealth for some other households.36 Figure 11 shows that slightly more than half of the top 5 percent of households have a share in a private business. The average value of these holdings is nearly $4 million. Only 14 percent of families in the next 45 have ownership in a private business, but for those that do, this type of wealth constitutes a substantial portion of their assets–the average amount of this business equity is nearly $200,000, representing more than one-third of their net worth. Only 3 percent of the bottom half of households hold equity in a private business, but it is a big share of wealth for those few.37 The average amount of this wealth is close to $20,000, 60 percent of the average net worth for these households.38

Owning a business is risky, and most new businesses close within a few years. But research shows that business ownership is associated with higher levels of economic mobility.39 However, it appears that it has become harder to start and build businesses. The pace of new business creation has gradually declined over the past couple of decades, and the number of new firms declined sharply from 2006 through 2009.40 The latest SCF shows that the percentage of the next 45 that own a business has fallen to a 25-year low, and equity in those businesses, adjusted for inflation, is at its lowest point since the mid-1990s. One reason to be concerned about the apparent decline in new business formation is that it may serve to depress the pace of productivity, real wage growth, and employment.41 Another reason is that a slowdown in business formation may threaten what I believe likely has been a significant source of economic opportunity for many families below the very top in income and wealth.

Inheritances

Along with other economic advantages, it is likely that large inheritances play a role in the fairly limited intergenerational mobility that I described earlier.42 But inheritances are also common among households below the top of the wealth distribution and sizable enough that I believe they may well play a role in helping these families economically.

Figure 12 shows that half of the top 5 percent of households by wealth reported receiving an inheritance at some time, but a considerable number of others did as well–almost 30 percent of the next 45 percent and 12 percent of the bottom 50. Inheritances are concentrated at the top of the wealth distribution but less so than total wealth. Just over half of the total value of inheritances went to the top 5 percent and 40 percent went to households in the next 45. Seven percent of inheritances were shared among households in the bottom 50 percent, a group that together held only 1 percent of all wealth in 2013.43

The average inheritance reported by those in the top 5 percent who had received them was $1.1 million. That amount dwarfs the $183,000 average among the next 45 percent and the $68,000 reported among the bottom half of households. But compared with the typical wealth of these households, the additive effect of bequests of this size is significant for the millions of households below the top 5 that receive them.

The average age for receiving an inheritance is 40, when many parents are trying to save for and secure the opportunities of higher education for their children, move up to a larger home or one in a better neighborhood, launch a business, switch careers, or perhaps relocate to seek more opportunity. Considering the overall picture of limited resources for most families that I have described today, I think the effects of inheritances for the sizable minority below the top that receive one are likely a significant source of economic opportunity.

Conclusion

In closing, let me say that, with these examples, I have only just touched the surface of the important topic of economic opportunity, and I look forward to learning more from the work presented at this conference. As I noted at the outset, research about the causes and implications of inequality is ongoing, and I hope that this conference helps spur further study of economic opportunity and its effects on economic mobility. Using the SCF and other sources, I have tried to offer some observations about how access to four specific sources of opportunity may vary across households, but I cannot offer any conclusions about how much these factors influence income and wealth inequality. I do believe that these are important questions, and I hope that further research will help answer them.